Celebrating their 10th Anniversary, Golden Gate Ventures (GGV) launched a report on the startup ecosystem in Southeast Asia. It elaborates essential points about the trend of the startup ecosystem in the last 10 years and its predictions in the next 10 years.

Founded in 2011, GGV has invested in around 60 startups and launched four fund initiatives. The investment thesis focuses on the growing presence of the consumer class in Southeast Asia. In Indonesia, its portfolio includes Alodokter, BukuWarung, Side, Alami, and GoPlay.

Startup ecosystem trend in the past 10 years

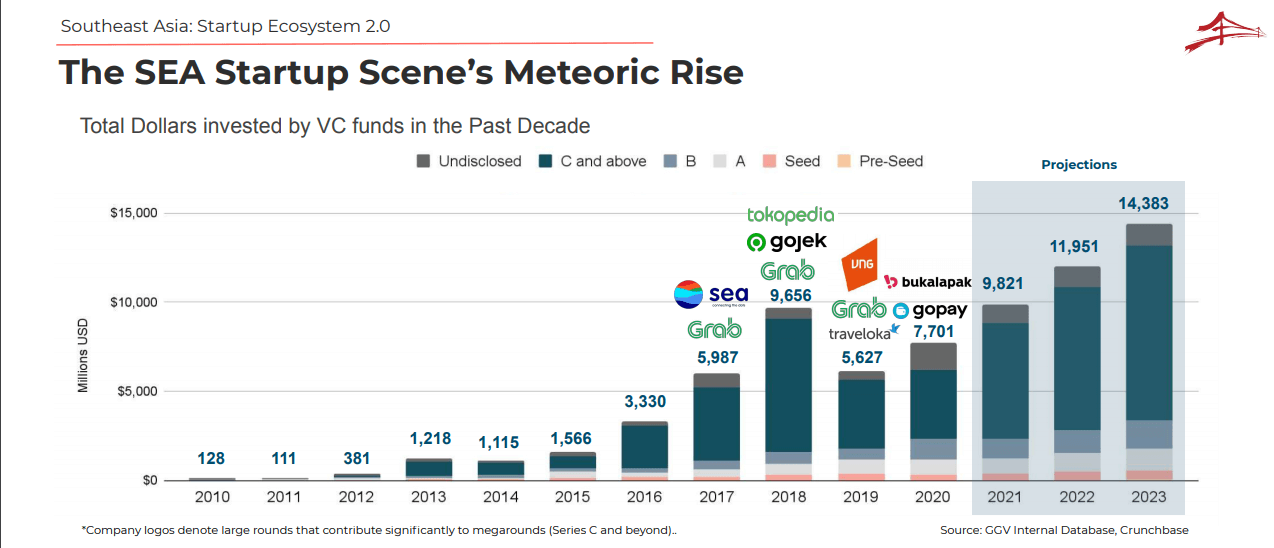

In the past decade, startups in the Southeast Asia region have experienced very fast growth. Especially in terms of capital inflows, it is estimated to have increased by 50x from $130 million in 2010 to $6.5 billion in 2020.

In its report, GGV noted more capital coming from the United States. These include Kleiner Perkins, Accel, KKR, Tiger Global and Warburg Pincus. In addition, funding also came from countries such as China and Japan. Not only are these countries leading large-scale funding, but these countries have also invested heavily in large companies in Southeast Asia.

The venture capitalists that later became leaders include Sequoia, Softbank, Tencent, and Alibaba. The business verticals that have received the most funding over the last 10 years are e-commerce, fintech, and entertainment. Meanwhile, GGV also noted that the fastest growing business verticals were food and logistics.

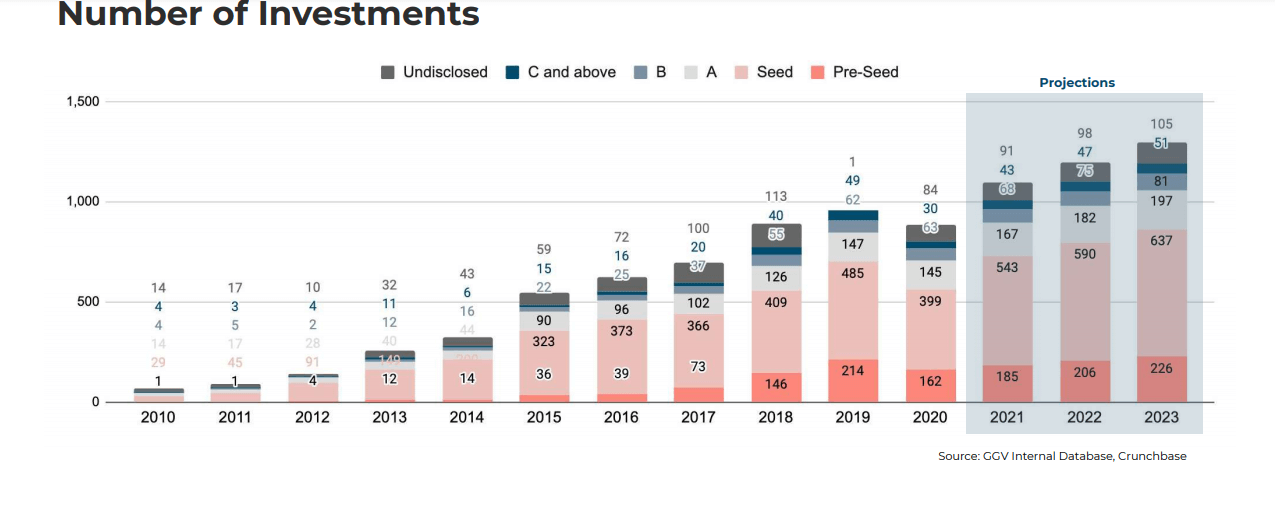

An interesting fact discovered by GGV is that the expansion in various stages of funding is getting more mature in line with the growing interest of regional and global investors for SEA. Series A round became the funding stage that experienced the fastest growth. Meanwhile, later stage funding (series C and above) experienced the highest jump (worth 100x) considering that there was no such round in the previous decade. The number of early stage and seed funding rounds has increased by up to 30x.

Another interesting point that GGV presented in its report is the increasing presence of Corporate Venture Capital (CVC) in Southeast Asia. There were only a handful of CVCs in 2010, which were usually branches of businesses established in family businesses, telecommunications companies, or super apps. Currently, there are more than 50 CVCs are listed.

In 2020, several CVCs have been involved in around 8.7% of all VC transactions and have led several funding rounds, especially in seed and series A. In Indonesia, several CVCs that are quite active in investing include MDI Ventures and Prasetia Dwidharma .

Indonesia also surpassed Singapore to become the country with the highest startups concentration with the best capital. On average, Indonesian startups have closed relatively larger funding rounds. Singapore recorded the largest VC capital is in 2010 (90%) but their share shrank to 40% in 2020.

Another captivating infornmation by GGV is that Indonesia has become a market demand for around 75% of unicorns in Southeast Asia, and is claimed to be the most successful market for investing in the Southeast Asian region.

Startup ecosystem trend in the next 10 years

In its report, GGV also conveys a number of trends in the startup ecosystem in the next 10 years. Among those is the increasingly widespread presence of social commerce. Its GMV is predicted to exceed $5 billion by 2025 and $25 billion by 2030 as it will continue to increase in e-commerce adoption, mixed with per capita GDP growth over the next decade.

In addition, another sector that is predicted to experience growth is healthtech. In this case, it is a platform that provides access to healthcare for a larger demographic, and improves infrastructure in Southeast Asia, especially after the pandemic.

Another prediction by GGV is the increasing number of IPO activities in Southeast Asia, which is expected to exceed 300 IPOs by 2030, as more local startups seek potential exits in the domestic public market.

Meanwhile, for Indonesia and Malaysia, it is estimated that there will be larger market growth for platforms that target Muslims. Indonesia and Malaysia’s market size will grow about 8x from its current size by 2030, including the Muslim lifestyle/halal economy in various industries such as fashion, food and finance.

Another trend that discussed in the report is that startups targeting media and entertainment will gain a stronger following and funding as the industry begins to shift its focus to digital solutions, including TV/film, live streaming, and esports. Funding in this area is predicted to exceed $700 million by 2030.

The large number of unbanked population in Southeast Asia creates huge opportunities that can trigger the growth of unicorn startups specifically for fintech. Potential services to be disrupted by fintech platforms include digital wallets, Neobanks, BNPL, and other forms of financing.

Mergers and acquisitions (M&A) activities are also predicted to increase in the next 10 years. As companies continue to compete for the top positions in its verticals, there will be more mega-mergers in Southeast Asia.

After Indonesia, which became the most targeted market by venture capitalists in the last 10 years, GGV predicts that within the next 10 years, Vietnam will become the targeted country for investors in Southeast Asia. Vietnam will emerge in 2022 as the premier startup ecosystem in Southeast Asia. This is visible with the increasing number of venture capitalists who then allocate their funds to invest in startups from Vietnam.

Meanwhile, for venture capitalists, it is predicted that within the next 10 years, the Assets Under Management (AUM) will be doubled. AUM has been increasing on a steady track over the last decade and it is estimated that it will exceed $300 billion by 2030.

–

Original article is in Indonesian, translated by Kristin Siagian

Gambar Header: Depositphotos.com